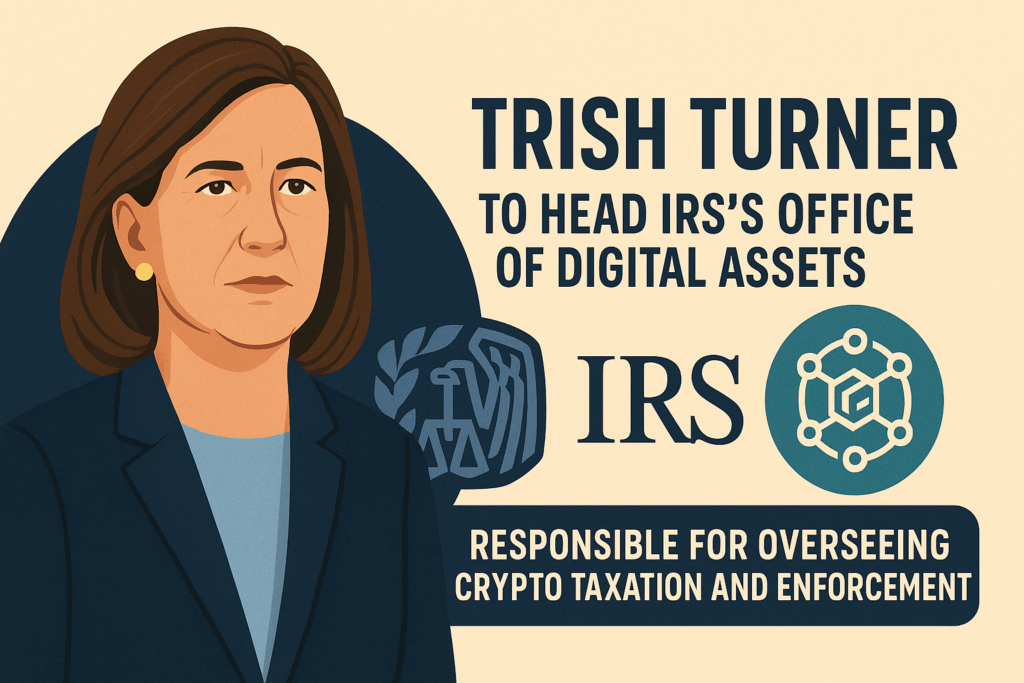

IRS Taps Veteran Trish Turner to Lead Crypto Division Amid Leadership Shake-Up and Shifting Regulatory Winds

Appointment of 20-year IRS official follows departure of private-sector crypto leads, signaling potential shifts in enforcement and policy under a new administration and internal agency pressures.

A Critical Juncture for IRS Crypto Oversight

The U.S. Internal Revenue Service (IRS) has appointed Trish Turner, an official with over two decades of experience within the agency, to spearhead its digital assets division. This significant personnel change, reported around May 6, 2025 , occurs as the agency confronts considerable internal and external pressures regarding the enforcement of cryptocurrency taxation.

Pay 0% Tax Legally — Start Your Tax-Free Strategy Today

Even in low-tax jurisdictions, most investors still overpay.

Our elite partner tax law firms specialize in advanced legal structures that can reduce your effective tax rate to as low as 0%, fully compliant, audit-ready, and tailored to your profile.

Crypto-friendly. International. Proven.

Turner’s appointment is more than a standard leadership rotation. It comes on the heels of the departure of Sulolit “Raj” Mukherjee and Seth Wilks, two executives recruited from the private sector to lead the IRS’s cryptocurrency unit. This transition in leadership at the IRS’s “Office of Digital Assets” is particularly noteworthy. It unfolds against a backdrop of a shifting political climate in Washington concerning cryptocurrency regulation and broader instability within the IRS itself. The move prompts questions about the future trajectory of U.S. crypto tax enforcement, the extent of political influence on regulatory agencies, and the IRS’s capacity to manage the intricacies of the rapidly evolving digital asset landscape.

The selection of an agency insider like Turner, contrasting with her predecessors who brought external industry experience, may signal a strategic recalibration. The previous leaders, Mukherjee and Wilks, were explicitly “private-sector experts” valued for their direct knowledge of the crypto industry. Their tenure, however, was brief, lasting “roughly a year” or “a little over a year”. In contrast, Trish Turner is a “veteran US Internal Revenue Service (IRS) official” with “over 20 years at the IRS” and, more specifically, “nine years supporting the service in several digital asset roles”. This pivot from external specialists back to long-term internal leadership could suggest a re-evaluation of the IRS’s approach. While individuals from the private sector offer fresh perspectives and specialized, current knowledge, an insider such as Turner contributes profound institutional understanding, established internal networks, and a deep familiarity with governmental processes. Consequently, Turner’s leadership might focus on more deeply embedding crypto enforcement within existing IRS structures and protocols. This could foster more sustained, though perhaps less agile, strategies, potentially reflecting a preference for stability and continuity after a period of reliance on external figures. This shift could also be a pragmatic response to the “very difficult environment” that federal employees reportedly face, implying that navigating the internal complexities of the IRS bureaucracy may be as critical as possessing niche crypto expertise.

The Departures: A Void at the Top of Crypto Enforcement

The leadership vacuum at the IRS’s crypto unit was created by the exits of Sulolit “Raj” Mukherjee and Seth Wilks around May 5, 2025. Mukherjee held the role of executive director of compliance and implementation, while Wilks served as executive director of digital asset strategy and development. Both individuals had joined the IRS in early 2024, bringing valuable experience from the cryptocurrency industry; Mukherjee was previously head of tax for Binance.US and held a senior position at ConsenSys, and Wilks was a former vice president at TaxBit. Their mandate included the development of crypto tax policies, spearheading the creation of the new Form 1099-DA for reporting digital asset transactions, and managing the agency’s engagement with the crypto sector.

The circumstances surrounding their departures offer insight into the pressures facing the agency. Wilks announced his exit on LinkedIn, alluding to a “very difficult environment” for federal employees and stating, “If stepping aside helps preserve someone else’s job, then I am at peace with the decision”. Mukherjee confirmed his departure separately to Bloomberg Tax. Some reports suggest their exits were linked to the government’s “DOGE Deferred Departure Plan” , an initiative reportedly part of a broader “government-wide cleanout” and efficiency drive under the Trump administration’s “Department of Government Efficiency” (DOGE). According to these reports, the officials were placed on paid leave until September, with the expectation that most would not return.

The departure of these executives after a relatively short period leaves a void in the specific private-sector expertise they were recruited to provide. Their contributions to key initiatives, notably the Form 1099-DA and the formulation of new crypto rules , were considered significant. The connection of these departures to the “DOGE Deferred Departure Plan” suggests that broader administrative restructuring may be at play. This initiative, aimed at reducing “bloated staffing left behind by the Biden administration” (under whom the IRS had expanded by approximately 20,000 workers ), and prioritizing “efficiency” , could have direct implications for specialized units. Wilks’ comment about his departure potentially “preserving someone else’s job” strongly hints at budget constraints or headcount reductions impacting the crypto unit. If such efficiency drives lead to the loss of crucial experts, it could inadvertently weaken the IRS’s ability to effectively regulate and tax the complex crypto sector, potentially undermining the very efficiency it aims to achieve.

Furthermore, the “very difficult environment” Wilks referenced , combined with reports of over 23,000 IRS employees expressing interest in resigning due to a reintroduced deferred resignation policy , indicates significant morale and stability challenges within the agency. Actions by the Trump administration, such as the controversial decision to share taxpayer data with Immigration and Customs Enforcement (ICE), which reportedly led to other top officials’ departures , contribute to this strained atmosphere. Such an environment could act as a deterrent for future private-sector experts considering government service, particularly in highly specialized and rapidly evolving fields like cryptocurrency. A diminished ability to attract or retain individuals with cutting-edge knowledge could compromise the government’s capacity to craft effective and informed policy and enforcement strategies, potentially widening the gap between regulatory capabilities and market realities.

Enter Trish Turner: A Veteran Takes the Crypto Reins

Trish Turner has been appointed to lead the IRS’s Office of Digital Assets. She is a long-serving IRS official, with a tenure exceeding 20 years at the agency. Her most recent position was Senior Advisor within the Digital Assets Office , also described as Senior Advisor for Digital Assets supporting the Digital Asset Project Office (DAIPO) in National Headquarters. Notably, Turner has dedicated nine years to various digital asset roles within the IRS, accumulating substantial experience in this specific domain.

Turner’s expertise is further evidenced by her active engagement in the field. She has been described as a “critical partner with domestic and international stakeholders, leveraging resources while sharing knowledge, data and best practices”. In public forums, she has discussed the utility of blockchain intelligence in combating financial crimes and has emphasized the necessity of proactive measures and robust public-private partnerships for tracing cryptocurrency transactions. Turner has also clearly articulated the IRS’s official position that digital assets are treated as property for federal tax purposes and has underscored the importance of the new Form 1099-DA in assisting taxpayers to understand their obligations and simplify reporting. Her involvement extended to the development of the Digital Asset Initiative Project Office (DAIPO), which was established in October 2022 to coordinate service-wide efforts on digital assets.

Her appointment suggests a degree of continuity, given her pre-existing senior advisory role within the IRS’s digital assets framework. However, her leadership style and strategic priorities may diverge from those of her predecessors, who came directly from the private sector. Turner’s extensive institutional knowledge could prove to be a significant stabilizing factor for the Office of Digital Assets, especially as the IRS navigates internal instability marked by potential mass resignations and external pressures from a new administration with a distinct regulatory philosophy. Unlike the previous crypto leaders who were relatively new to the federal system , Turner possesses a deep understanding of the agency’s culture, operational realities, and bureaucratic intricacies. This background may enable her to implement strategies more effectively within the existing framework, even if these strategies are less disruptive than what external hires might have envisioned. Her stated focus on taxpayer understanding could also represent a pragmatic approach to enhancing compliance in a notoriously complex area.

Moreover, Turner’s experience in international engagement is particularly relevant. The cryptocurrency market is inherently global, making international cooperation essential for effective regulation and tax enforcement. This is underscored by initiatives like the OECD’s Crypto-Asset Reporting Framework (CARF). While the previous administration was involved in international efforts to coordinate crypto regulation, the current Trump administration’s approach to such cooperation might differ. Turner’s established role as a “critical partner with domestic and international stakeholders” and her advocacy for partnerships in tracing transactions could be vital in ensuring the IRS’s digital asset strategy remains aligned with global best practices and maintains crucial information-sharing channels, irrespective of broader shifts in U.S. foreign policy or domestic regulatory stances. This international perspective is indispensable for tackling tax evasion that often exploits the cross-border nature of crypto transactions.

The Shifting Sands: Crypto Regulation in the Current Political Climate

The regulatory environment for cryptocurrencies in the United States is undergoing a significant transformation, heavily influenced by the current Trump administration, which commenced in January 2025. There has been a discernible shift towards a more “pro-crypto” stance , characterized by efforts to scale back regulations perceived as overly burdensome to innovation in the digital asset sector.

A key example of this shift is the repeal of the controversial IRS DeFi broker rule. This rule, had it taken effect, would have significantly expanded tax reporting requirements to include Decentralized Finance (DeFi) platforms, mandating disclosure of gross proceeds from crypto sales and taxpayer information. President Trump signed the congressional resolution that nullified this rule. Further signaling a softer approach, the Securities and Exchange Commission (SEC) has reportedly dropped or paused over a dozen enforcement cases against crypto companies , and the Department of Justice announced the dissolution of its dedicated cryptocurrency enforcement unit. Additionally, President Trump issued an executive order aimed at creating a cryptocurrency working group to propose new regulations and explore the establishment of a U.S. crypto reserve.

Internally, the IRS is grappling with substantial pressures. Reports indicate that over 23,000 IRS employees have expressed interest in resigning following the Trump administration’s reintroduction of a deferred resignation policy. This potential exodus raises serious concerns about staffing levels, employee morale, and the agency’s overall capacity to fulfill its mandates, including complex areas like crypto enforcement. The administration’s “Department of Government Efficiency” (DOGE) is also actively pursuing measures to reduce federal staffing levels.

Despite this potentially more lenient regulatory climate and internal challenges, the IRS continues to underscore the importance of crypto tax compliance. Taxpayers remain obligated to report all digital asset transactions accurately. The agency has, in recent years, increased its focus on cryptocurrency, leading to more audits and criminal probes targeting digital asset transactions. Furthermore, the implementation of the new Form 1099-DA for broker reporting is moving forward. This form, a key project for the recently departed executives , will require brokers to report gross proceeds for transactions occurring from January 1, 2025, with basis reporting for certain assets to follow for transactions from January 1, 2026.

This situation presents a complex operational environment for the IRS’s Office of Digital Assets. On one hand, the administration is actively “scaling back regulations perceived as burdensome” and has facilitated the repeal of the DeFi broker rule. The Department of Justice has even disbanded its crypto enforcement unit , signaling a broader deregulatory push. On the other hand, the IRS is simultaneously advancing significant new tax reporting requirements through Form 1099-DA , a measure designed to increase visibility into crypto transactions for tax purposes. The agency also continues its own audits and investigations. Trish Turner, as the new head, must navigate this landscape, implementing these new reporting requirements while her agency potentially faces resource reductions and operates under an administration that might be philosophically inclined to lessen regulatory burdens. This inherent tension means Turner will need to balance the administration’s deregulatory rhetoric with the fundamental statutory mandate to collect taxes and the practical necessity of robust information reporting to achieve this effectively. The success of Form 1099-DA thus becomes even more critical as a primary tool if other enforcement avenues are diminished. This could lead to a highly focused, data-driven enforcement strategy centered on reported information, rather than broader, more resource-intensive investigations.

The administration’s “efficiency” drive, spearheaded by the DOGE initiative , coupled with the potential departure of 23,000 IRS employees , poses a threat to the agency’s human capital and specialized expertise. Effective crypto tax enforcement demands not only specialized knowledge and sophisticated analytical tools but also sufficient personnel for audits, investigations, and taxpayer service. The tax gap related to digital assets is estimated to be substantial, with some studies suggesting it could be at least $50 billion. Addressing this gap necessitates sustained investment in enforcement capabilities. If the pursuit of “efficiency” translates into indiscriminate cuts that impair the IRS’s ability to understand and police the crypto space, it could prove counterproductive. A weakened IRS may struggle to implement new reporting regimes effectively, analyze the collected data, and pursue non-compliance, potentially leading to an even larger crypto tax gap in the long run. This outcome would undermine the administration’s own potential revenue objectives and the core principle of fair taxation. Turner will face the considerable challenge of achieving compliance goals with potentially diminished resources.

The following table provides a timeline of key recent events influencing IRS digital asset policy and leadership:

Table 1: Key IRS Digital Asset Leadership and Policy Timeline

| Date/Period | Key Personnel/Leadership | Key Policy/Regulatory Development | Administrative Context | Relevant References |

|---|---|---|---|---|

| Early 2024 | Sulolit Mukherjee & Seth Wilks hired | Brought in from private sector to develop crypto tax policies, lead Form 1099-DA creation | Biden Administration focus on crypto expertise | |

| Jan 2025 | Trump Administration begins second term | Signals “pro-crypto” stance, initiates “Department of Government Efficiency” (DOGE) | Shift in regulatory philosophy | |

| Jan 2025 | N/A | Executive order for crypto working group & U.S. crypto reserve | Trump Administration initiative | |

| April 2025 | N/A | President Trump signs resolution repealing IRS DeFi broker rule | Trump Administration scales back perceived burdens | |

| May 5, 2025 | Sulolit Mukherjee & Seth Wilks depart | Departures linked to “DOGE Deferred Departure Plan” and “difficult environment” | Trump Admin efficiency drive, IRS internal pressures | |

| May 6, 2025 | Trish Turner appointed Head of Office of Digital Assets | Veteran IRS official with extensive digital asset experience takes leadership | IRS seeks stability amidst change | |

| Jan 1, 2025 (onw.) | Trish Turner leads Office of Digital Assets | Implementation of Form 1099-DA begins (gross proceeds reporting for 2025 transactions) | Continued IRS focus on tax compliance | |

| Jan 1, 2026 (onw.) | Trish Turner leads Office of Digital Assets | Form 1099-DA basis reporting for certain assets acquired and held with same broker (for 2026 transactions) begins | Phased rollout of new reporting requirements |

The IRS’s Digital Asset Framework and Turner’s Role

Trish Turner will now head the IRS’s Office of Digital Assets (ODA) , the primary unit responsible for overseeing crypto taxation and enforcement. This office was previously co-led by the departed executives, Mukherjee and Wilks. Closely related is the Digital Asset Initiative Project Office (DAIPO), established in October 2022. The DAIPO serves as a coordinating body for service-wide digital asset efforts, including the development of crucial forms like the 1099-DA, official guidance, information systems, and public outreach activities. Turner herself was previously a Senior Advisor supporting this project office , indicating her familiarity with its strategic objectives. The DAIPO’s overarching goal is to operationalize digital asset-related work under a cohesive, agency-wide strategy.

The IRS maintains a clear stance on the tax treatment of digital assets: they are considered property for federal tax purposes, not currency. Consequently, transactions involving digital assets can result in capital gains or losses for taxpayers. Furthermore, income derived from digital assets—such as through mining, staking, or receiving them as payment for goods or services—is taxable. To enhance awareness and improve reporting, the IRS has expanded the digital asset question that appears on various tax forms, including Form 1040 (individual income tax), Form 1065 (partnerships), and Form 1120 (corporations).

The new Form 1099-DA is a cornerstone of the IRS’s evolving reporting framework for digital assets. Its implementation is phased:

- Brokers will be mandatorily required to report gross proceeds for digital asset sales and exchanges effected in the calendar year 2025, with these reports due to the IRS and taxpayers in 2026.

- Reporting of tax basis for certain digital assets—specifically those acquired from and held with the same broker on or after January 1, 2026—will be required for transactions occurring in 2026, with these reports due in 2027. The term “broker” under these new rules encompasses U.S. custodial digital asset trading platforms, digital asset payment processors, certain digital asset hosted wallet providers, and operators of digital asset kiosks. Notably, the initial set of final regulations does not cover non-custodial brokers or those operating within the DeFi space; further guidance for these entities is anticipated. Trish Turner has publicly stated that these new reporting rules are intended to help taxpayers better understand their obligations and to simplify the process of reporting their digital asset activity.

Turner’s prior involvement with the DAIPO, the coordinating body for service-wide digital asset strategy and tool development , and her new role as head of the ODA, the primary operational and enforcement arm , could foster stronger alignment between these critical components. The success of the IRS’s crypto strategy hinges on seamless coordination between policy and tool development (DAIPO) and operational execution and enforcement (ODA). Her experience bridging these areas may lead to more coherent policy implementation, better-designed tools that meet operational needs, and a more unified approach to crypto tax administration.

However, the phased implementation of Form 1099-DA and its initial exclusion of DeFi brokers mean that significant information gaps and compliance burdens will persist. The now-repealed “DeFi broker rule” was specifically designed to cover this decentralized segment. Taxpayers and practitioners will continue to face complexities in tracking basis, especially for assets moved between various wallets and exchanges or those acquired before the new rules take full effect. While the IRS has provided some relief through safe harbor provisions for basis allocation, such as Revenue Procedure 2024-28 , the challenge remains. Turner’s office will be responsible for navigating this transitional period, educating taxpayers and brokers, and eventually integrating reporting for the DeFi sector. The goal of achieving comprehensive third-party reporting, which is known to significantly improve tax compliance rates , remains a substantial hurdle in the decentralized portions of the crypto ecosystem. Turner’s expressed optimism that Form 1099-DA will eventually include all necessary information for taxpayers will be tested against these ongoing complexities.

Implications for the Crypto Industry and Taxpayers

The appointment of Trish Turner and the evolving regulatory landscape carry significant implications for both the cryptocurrency industry and individual taxpayers. For the crypto industry, Turner’s leadership might translate into a more predictable, albeit potentially less flexible, interaction with the IRS compared to leaders who had more direct ties to the private sector. Her stated emphasis on fostering public-private partnerships could be viewed positively if it leads to constructive dialogue and clearer guidance. However, the industry will likely remain wary of increased scrutiny, even under an administration that professes a “pro-crypto” stance. The ongoing implementation of Form 1099-DA will undoubtedly require substantial compliance efforts and system adjustments from brokers operating in the U.S. market.

For taxpayers, Turner’s articulated goal of leveraging Form 1099-DA to simplify reporting and help individuals better understand their tax obligations is a welcome prospect. Clearer reporting could reduce inadvertent errors and the burden of complex calculations. Nevertheless, the broader environment of IRS instability, potential staffing shortages, and shifting political winds could introduce elements of uncertainty. The fundamental requirement remains: taxpayers must accurately report all income and transactions related to digital assets.

Turner will be tasked with a delicate balancing act. She must reconcile the administration’s apparent desire for a lighter regulatory touch on innovation with the IRS’s core mission of ensuring tax collection and enforcing compliance in a sector known for its complexity and, at times, significant non-compliance.

Given the potential resource constraints stemming from widespread resignations and government efficiency drives , coupled with an administration that signals a softer stance on broad regulations but still expects tax compliance , Turner’s leadership might pivot towards a more data-driven and surgically precise enforcement strategy. Her experience with data analytics and blockchain intelligence , along with the IRS’s ongoing investment in these tools , supports this possibility. The massive new dataset generated by Form 1099-DA will be a critical asset. Instead of relying on broad, resource-intensive crackdowns, the IRS could increasingly use advanced analytics on reported data and other blockchain intelligence to identify high-risk areas of non-compliance with greater accuracy. This “smarter, not harder” approach could be a pragmatic way to maximize enforcement impact with limited resources, aligning with both the mandate for efficiency and the pressing need to address the crypto tax gap. However, such an approach also brings to the forefront important considerations regarding data privacy and the potential for algorithmic bias in selecting targets for enforcement.

Conclusion: Navigating Uncertainty with a Steady Hand?

Trish Turner assumes leadership of the IRS’s digital asset division at a moment of considerable upheaval. Her tenure begins against a backdrop of high-profile leadership departures, shifting political pronouncements on cryptocurrency regulation, significant internal instability within the IRS, and the enduring complexities inherent in the taxation of digital assets.

Despite these formidable challenges, Turner brings notable strengths to the role. Her deep and lengthy experience within the IRS, coupled with nearly a decade of specialized knowledge in digital assets and a track record of international engagement, provides a solid foundation for steady and informed leadership. She understands the agency’s internal workings and the nuances of the digital asset space from a regulatory perspective.

Pay 0% Tax Legally — Start Your Tax-Free Strategy Today

Even in low-tax jurisdictions, most investors still overpay.

Our elite partner tax law firms specialize in advanced legal structures that can reduce your effective tax rate to as low as 0%, fully compliant, audit-ready, and tailored to your profile.

Crypto-friendly. International. Proven.

The cryptocurrency industry, tax professionals, and individual taxpayers will be closely observing how Turner navigates this multifaceted environment. Her success will be measured by her ability to effectively implement the new, complex reporting requirements associated with Form 1099-DA, maintain appropriate enforcement pressure where necessary to ensure compliance, and adapt the IRS’s strategies to the continuously evolving technological and market landscape of digital assets. The central question is whether an experienced insider, well-versed in the agency’s culture and processes, can bring stability and effective oversight to a domain still characterized by rapid innovation, regulatory ambiguity, and significant political crosscurrents.

The IRS’s journey in addressing cryptocurrency taxation is a long-term endeavor, evolving from initial guidance like Notice 2014-21 to the establishment of specialized units such as the DAIPO and the development of comprehensive reporting regimes like Form 1099-DA. While leadership changes and shifts in political administrations can create short-term turbulence, the fundamental necessity of integrating digital assets into the existing tax system persists. Turner, with her extensive career at the IRS, likely appreciates that establishing robust tax administration for a novel asset class is a marathon, not a sprint. Her appointment may signify a commitment to the long-term institutionalization of crypto tax compliance within the IRS. The focus could be on deeply embedding these processes within the agency, thereby ensuring resilience against future political winds or personnel changes. This suggests a strategic move towards treating cryptocurrency less as an exotic outlier and more as a standard, albeit complex, component of the overall tax landscape.